CBDT via notification dated 12th April 2019 has introduced certain changes in Form 16 so as to make it more informative and regularise with Income tax returns. The said notification is effective from 12th May 2019. Part A and Part B have now been made more informative for users.

The season of return filing is again back but are you (taxpayers) ready to furnish Income tax returns? This time its FY 2018-19 and slabs of incomes and rate of tax will be as per Finance Bill 2018.

CBDT has come out with Forms ITR 1 and ITR 4 only till now of which only ITR 1 is one which can be used by salaried people and the biggest tax base of the country. Refer last blog about the additional information sought in those forms. Click here to read

Similar to prior years when Form 16 and columns of salary were captured almost similar details, this year as well changes are introduced in form 16 to streamline the details required in Income tax return with the data appearing in Form 16.

To see the changes introduced, let’s begin with the basics.

1. What is Form 16?

Under Income Tax Act, every employer is required to furnish a certificate to TDS deducted from the salary and deposited with the Income Tax authorities to an employee in a prescribed format called Form 16. It contains the details which are needed to be captured in income tax return form as well.

Due Date: Unlike other TDS certificates, Form 16 is issued annually, on or before 15th June of the year, immediately following the financial year in which tax is deducted. i.e. due date for issue of Firm 16 for FY 2018-19 is 15th June 2019.

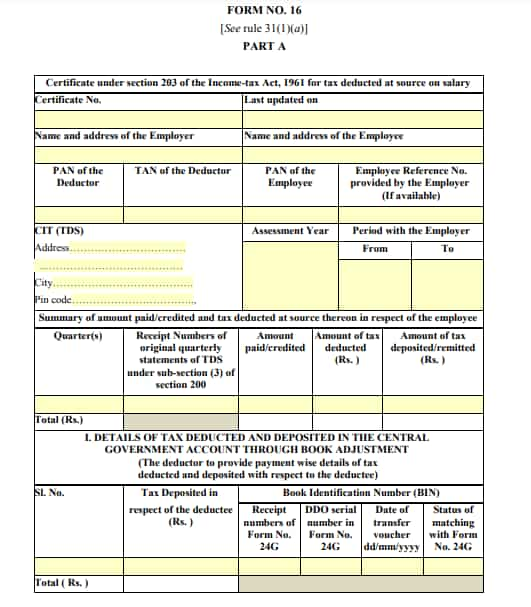

Form 16 is essentially divided into two parts:

- Part A: containing details about the tax deducted during each quarter of the year.

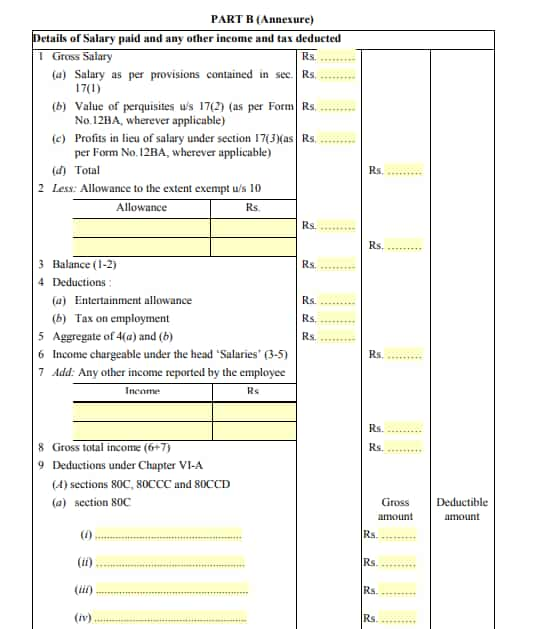

- Part B (Annexure): Details of salary paid and any other income and tax deducted

Such certificate is issued containing signatures of the employer. Employer may also use Digital Signatures as per his discretion.

In case you lose your Form 16, a duplicate can be issued by your employer.

A sample of Form 16 is shown below:

2. What’s new in Form 16 being talked about?

Recently, CBDT via notification dated 12th April 2019 has introduced certain changes in Form 16 so as to make it more informative and regularise with Income tax returns. The said notification is effective from 12th May 2019.

Changes:

There is no change in Part A of Form 16 which contains details of tax deducted and deposited. Significant and awaited changes have been introduced in Part B.

Change 1: Amount of Salary from any other employer received during the year: Earlier details of salary received form any previous or any other employer was required to be furnished only in Form 12BB while submitting declarations to enable the employer determine the TDS to be deducted from salary of the employee.

Change 2: Details of allowances exempt under section 10(5): Earlier there was no designated allowance/ sequence or heading under which such exempt allowances had to be mentioned in Form 16, however now with the reduction in the possible allowances available, amount of following exempt allowances are to be specifically shown in the fields highlighted against them:

- Travel concession or assistance under section 10(5)

- Death-cum-retirement gratuity under section 10(10)

- Commuted value of pension under section 10(10A)

- Cash equivalent of leave salary encashment under section 10(10AA)

- House rent allowance under section 10(13A)

Amount of any other exemption under section 10: This has to be mentioned with any other applicable clause applicable with the amounts.

Change 3: Field mentioning standard deduction under section 16(ia) has been introduced in accordance with the amendment for grant of standard allowance of Rs. 40,000 p.a. for FY 2018-19 was introduced in Finance Bill 2018.

Change 4: Now under Clause 7, ‘Other incomes reported by employee” which are to disclosed to employer as a part of Form 12BB, there is a specific field for income or admissible loss from house property reported by employee offered for TDS and income under the head Other Sources offered for TDS. Earlier, there was no specific guideline on the nature of income to be mentioned on Form 16.

Change 5: Under the clause for deductions under Chapter VI-A, description of each deduction claimed by employee are mentioned which will make understanding the certificate easier.

Change 6: Addition of a specific clause mentioning Rebate u/s 87A which was earlier not disclosed.

These are appreciable changes which will facilitate not only detailed presentation of deductions and allowances being received by an employee but also make it easier for an employe to understand his salary structure and tax declarations.

Need any clarifications? Have a query?

Write to us at info@taxtellers.com

Regards,

TheTaxTellers Team